2026 Market Outlook: High Risk High Reward

- Daniel Lee

- Jan 1

- 6 min read

With the world ushering back an era of cheap money in 2026, here are three key themes investors should watch for in the markets this year.

US: Rate Cuts & "Quantitative Easing"

On Rate Cuts:

Despite having an explicit indication by Federal Reserve Chairman Jerome Powell that the Fed may now hold the rates for some time, given that they “cannot fully trust” (yes, he said that) the key economic reports on jobs and inflation due to the governmental shutdown, odds are that the Federal Reserve will continue its path to cut rates further in 2026.

The reason for having a contradictory view is due to the increasing politicisation of the Federal Reserve, which is set to test the Fed’s independence in 2026. Given that Jerome Powell's tenure expires on 15 May 2026, and considering that President Trump is likely to install someone aligned with his views, it is likely that the board's vote will be skewed towards favouring further rate cuts, regardless of the economic conditions or data.

Based on the most recent dot plot, the committee is pointing towards a single rate cut in 2026, which is set to bring the rates down to 3.25% but the market is expecting two rate cuts, which would bring rates down to 3.00% which is close to the widely considered neutral rate (neither expansionary nor contractionary to the economy).

On Quantitative Easing:

Having ceased the quantitative tightening on 1st December 2025, the Federal Reserve has announced that it will soon begin purchasing short-term treasury bills of around $40billion per month under the guise of “maintaining an ample supply of reserve” ahead of the 15 April 2026 tax payments under the Reserve Management Purchase (RMP) instead of calling it Quantitative Easing.

In practical terms, however, this would bring the total injection to $60billion per month into the markets, which does have a similar easing impact as that of the quantitative easing. Similar to the previous point on rate cut, while the ongoing RMP is supposed to be temporary, there might be a good chance that it continues on longer than expected – especially when Jerome Powell’s tenure is up.

Why does this matter

The impact comes in two forms – a further erosion of the USD long-term strength and a quick dopamine boost to an already overvalued equities market.

On the topic of a short-term equity boost:

In the short term, increased money supply is likely to flow into the equities market, driving prices higher as additional capital competes for a finite number of quality companies.

On the topic of the strength of the USD:

With an already worsening perception of the fiscal irresponsibility of the Federal Government, any further increase in money supply via expansionary monetary policy and a cheap money environment will inevitably result in a weaker USD moving in the future.

In fact, the consensus now is that we may see a USD/SGD parity in the next 15-20 years, following the same pace of USD depreciation as we’ve previously experienced in the past. Given that the majority of the global investments are denominated in USD, this will ultimately erode our investment returns in the form of FX losses.

The silver lining with respect to the weaker USD may come in the form of higher earnings by US-listed companies with foreign market exposure in the form of higher FX gains. As such, this will form a positive catalyst that may push equity prices higher which will help offset any FX losses in the future.

Like it or not, FX risk is an unavoidable risk that we as international investors will have to deal with. That said, this can be managed with proper diversification and an eventual transition from international equities to domestic equities and bonds as we move towards our retirement goals.

Global: Cracks In AI Hype?

If there’s anything that may result in an immediate correction to downright a financial crisis at the moment, it will be the unravelling of the AI hype.

Given that the growth in the AI space is supported by circular financing loops and excessive private credit build-up, these mechanics have potentially led to the inflation of revenue metrics, distortion of operational cash flows, and accumulation of hidden debt risks on corporate balance sheets.

Should market confidence erode, the demand for AI infrastructure fall short of expectations, GPU prices fall faster than expected, or a highly intertwined company experiences financing or liquidity difficulty, a simultaneous unwinding of these interconnected financial structures could precipitate a severe market correction or credit crisis, distinct from, yet equally potent as, the 2000 bust.

The primary risk here is not merely an equity correction, but a credit-driven cascade where stress in the highly leveraged infrastructure sector compromises the financial integrity of the core technology suppliers.

Why does this matter

As both the economy and the stock market are currently underpinned by the AI narrative, adverse developments in this sector would likely undermine investor confidence. This effect could be amplified by weakening economic indicators, resulting in a negative feedback loop that drives equity prices lower.

While it is highly likely that the government would step in and bail out failing companies in order to control the damage in the financial markets and prevent a systemic collapse (similar to that of 2008), the unwinding of existing contracts and revenue performance obligations will negatively impact the earnings of companies.

This will result in a need to re-evaluate the fair value of these companies (which accounts for a huge portion of the indexes), thereby causing a correction in the share prices even if the current valuations persist (which is highly unlikely in an environment where investor confidence is low).

Asia: Improving Confidence & Demand For Diversification

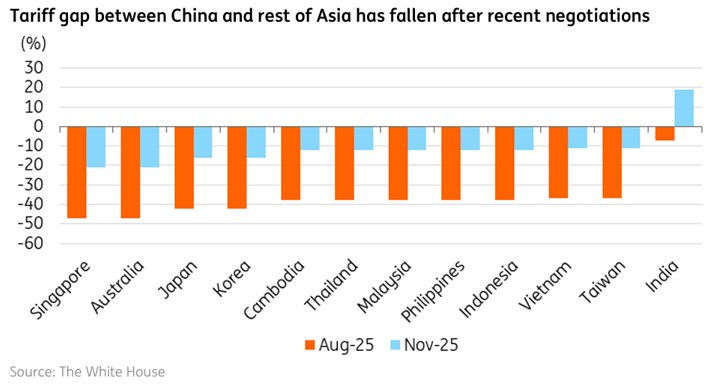

Asia’s economic resilience has been notable despite the ongoing trade war initiated by Donald Trump in April 2025. This strength is partly due to the formation of new trade alliances, both within the region and with Europe, as well as increased tech-related exports.

Uncertainty regarding political instability and global trade appears to have peaked in 2025, with markets now stabilizing around established tariff levels following several rounds of negotiations with the United States.

This resilience of Asian economies has actually corresponded to higher investment fund inflows into Asian markets in 2025. This trend is expected to continue and even improve further moving into 2026, driven largely by the long-term prospects of the region, coupled with the increasing demand to diversify away from overvalued developed markets.

Why does this matter:

Provided that global markets remain stable and investor confidence is not undermined by significant negative events, Asia and emerging markets are expected to maintain their upward momentum.

These regions offer stronger long-term earnings growth potential compared to developed markets, and valuations remain attractive. However, increased capital inflows may lead to heightened volatility if sentiment shifts as these inflows can be quickly unwound as funds flow out of the region in a flight to safety.

Overall, current valuations and capital flows indicate that Asia’s markets have further upside in 2026, assuming earnings meet expectations and no major disruptions occur.

Conclusion: High Risk High Reward

2026 presents a dynamic investment landscape, shaped by distinct positive and negative catalysts.

If the AI sector remains stable and avoids triggering a credit-driven downturn, developed markets are likely to trade sideways until earnings improve, while developing markets may see upward momentum as capital seeks better risk-return profiles.

The prevailing environment of low interest rates and reduced geopolitical uncertainty is expected to encourage business investment and hiring, supporting economic growth. However, these favorable conditions could be quickly reversed if significant disruptions emerge within the AI industry, with potential spillover effects on the broader economy and financial markets.

Outside of these short-term developments, the long-term mega trends continue to be in place and as such as long-term investors we should adhere to our strategy and manage our asset allocation in accordance with our financial plan.

Read more: 2025 Portfolio Review

Daniel is a Licensed Independent Financial Consultant with MAS and a Certified Financial Planner (CFP®).

Connect with me on social media platforms to receive updates on future content! You can also slide into my DMs if you have any questions :)

Disclaimer:

This article is meant to be the opinion of the author

This article is for information purposes only

This article should not be seen as financial advice

This advertisement has not been reviewed by the Monetary Authority of Singapore

![Is AIMS APAC REIT A Good Buy In 2026? [Fundamental Analysis]](https://static.wixstatic.com/media/5dc7f7_693c8bcadb39413385741ec58abd8a27~mv2.png/v1/fill/w_1277,h_720,fp_0.50_0.50,q_35,blur_30,enc_avif,quality_auto/5dc7f7_693c8bcadb39413385741ec58abd8a27~mv2.png)

![Is AIMS APAC REIT A Good Buy In 2026? [Fundamental Analysis]](https://static.wixstatic.com/media/5dc7f7_693c8bcadb39413385741ec58abd8a27~mv2.png/v1/fill/w_972,h_548,fp_0.50_0.50,q_95,enc_avif,quality_auto/5dc7f7_693c8bcadb39413385741ec58abd8a27~mv2.png)

![Is Mapletree Logistics Trust A Good Buy In 2026? [Fundamental Analysis]](https://static.wixstatic.com/media/5dc7f7_e7e6039bedd8473ba689d55789a5a586~mv2.png/v1/fill/w_1277,h_720,fp_0.50_0.50,q_35,blur_30,enc_avif,quality_auto/5dc7f7_e7e6039bedd8473ba689d55789a5a586~mv2.png)

![Is Mapletree Logistics Trust A Good Buy In 2026? [Fundamental Analysis]](https://static.wixstatic.com/media/5dc7f7_e7e6039bedd8473ba689d55789a5a586~mv2.png/v1/fill/w_972,h_548,fp_0.50_0.50,q_95,enc_avif,quality_auto/5dc7f7_e7e6039bedd8473ba689d55789a5a586~mv2.png)

Comments