Hospital Insurances Changes [April 2026]

- Daniel Lee

- Apr 12

- 11 min read

Updated: Apr 16

This article is written for my clients. If you are not my client but choose to read this article, please note that this is not financial advice. Please speak to your financial advisor before making any decision.

Another year, another round of changes applied to our hospitalisation insurance.

This time around, we’ve seen:

Higher prices for base plans, which apply to everyone

Changes in

The benefits of co-payment riders, which only apply to clients who purchased their hospitalisation insurance after 27 November 2025

premium of older riders, which applies to existing policyholders

In other words, if you’ve purchased your hospitalisation insurance before 27 November 2025, the benefit changes in the co-payment rider do not affect you, and you will continue to be insured for the deductibles with a lower co-payment cap.

All changes are effective starting from April 2026.

That said, it is likely that this round of changes may also be imposed on existing policyholders in the future. We’ve seen this happen when the government initiated the mandate to impose at least 5% of co-payment (which is the rider that we’re currently only) and the removal of the ability for hospitalisation plans to have 100% payout.

In this article, I’ll run you through

Changes To Hospitalization Plan

New Co-Payment Rider Introduced

Increase In Premium For Older Riders

Its implications and the viability of a hospitalisation insurance

Non-CDL Cancer Drug List Coverage

Likelihood of Utilising Non-CDL

Likely Duration of Treatment & Estimated Cost

Verdict For The Use Case Of Newer Riders

Actions you consider taking moving forward if you're covered for

For those who are too lazy to read, I'm sorry, but you need to read this article, as this round of changes are quite drastic and may change the way you approach healthcare financing moving forward. So no TLDR for you this round. ヘ( ̄ω ̄ヘ)

1. Changes To Hospitalisation Plan

1.1 Higher Base Plan Premium

Regardless of when you purchase the policy, nobody can escape the first implication of this round of changes: a higher premium in the base integrated shield plan.

For NTUC Income or HSBC Life in particular, this is the increment in base plan premiums for these two companies across the Public and Private hospitalisation coverage.

Unfortunately, unlike previous rounds of premium hikes that impacted mostly the private hospitalisation area, this round of hikes affected all levels of policyholders and is not just limited to those covered up to the private hospitalisation coverage.

That said, due to the nominal difference between private hospitalisation and public A ward hospitalisation coverage, the nominal increase in price is still higher in the private hospitalisation category despite having similar or lower levels of percentage increment.

1.2 Changes To Co-Payment Rider

1.2.1 New Co-payment Rider Introduced

As per the government’s instruction, all co-payment riders sold from April 2026 onwards

will not cover the deductibles and

have a higher co-payment cap of $6,000/yr instead of the previous $3,000/yr.

What this means is that as policyholders, our out-of-pocket expenses will be higher while the total insurance payout will be lower.

To put it more bluntly - MOH Don’t sue me - the usefulness of a hospitalisation plan now is solely limited to more catastrophic items and high hospital bills, and less useful (I’d argue useless even) when dealing with heavily subsidised treatments or low hospital bills.

I’ll elaborate on this in the implications section below as we examine the most common hospitalisation causes and the likely cost associated with the treatment.

Following the removal of coverage for deductibles and a higher co-payment limit, the premiums for the new versions of riders have also decreased by the following amount, listed in the table below, compared to the older riders:

1.2.2 Increase In Premiums For Older Rider

Unfortunately for us existing policy holders, apart from the increase in premiums for the base plan, we’re also slapped with another round of increase in premiums for the existing riders that we’re on.

For this round of changes, we’ve seen the price increase for HSBC Life and not NTUC Income.

That said, it is likely that this trend of premium increase in older riders would continue – either due to medical inflation or due to the fact that insurers would like to price people to the newer plan instead.

2. Implications of the changes

If I were to isolate the miscellaneous benefits and only focus on the core benefits, the use case of a rider lies in terms of their ability to:

Cover deductibles

Limit co-insurances

Lower co-insurance percentage from 10% to 5% (depending on the company)

Provide coverage for non-CDL benefits

With the first two core benefits being nerfed, the value of retaining the rider is now being questioned.

To answer the question of whether it is still worthwhile to continue financing for the rider, we’ll have to examine the likelihood of utilising the benefits and assess the cost associated with it versus other options such as self-financing or alternative financing using a life insurance.

2.1 Rider’s Role In Limiting Co-Payment Exposure

Based on the Ministry of Health’s data (2023 – 2025), here’s the average cost for the most common cause for hospitalization:

A critical limitation of published MOH bill size data is that it captures only single inpatient episodes - one hospital stay from admission to discharge. It does not consider pre & post hospitalization bills, which add up across the patient’s healthcare journey.

For chronic or complex conditions, the total financial outlay throughout the treatment journey is significantly higher, encompassing multiple chemotherapy cycles, intensive rehabilitation, or lifelong maintenance care.

A rough estimate of the all-in annual or total cost throughout the recovery journey for the common conditions is laid out in the table below:

Personal Verdict: Through this exercise, what you’d realise is that for the larger part outside of cancer care, the value of the rider in the areas of co-insurance limitation (5% or 10% capped at 6,000 per year) is questionable for their corresponding cost.

This brings me to the other value of having a rider which was only introduced in September 2022, the non-CDL benefit.

2.2 Non-Cancer Drug List (CDL) Coverage

As a refresher, Singapore's Cancer Drug List, maintained by MOH and updated three times annually, covers approximately 376 clinical indications, representing around 90% of HSA-approved cancer treatments.

The drugs that fall outside the CDL creates the critical coverage gap as patients are expected to either self-finance the cost or rely on insurance coverages (Critical Illness Payout from life insurances or non-CDL coverage from Shield Plan Riders).

Drugs fall under non-CDL classification for several distinct reasons:

The manufacturer has not offered a price meeting MOH cost-effectiveness threshold

Off-label use (CDL for one condition but non-CDL for another)

Indications not yet approved by HSA

This presents us with two layers of risks that we have to deal with. Firstly, what are the odds of us utilising a non-CDL drug as part of our treatment? Secondly, what will the duration be for a typical treatment and the estimated total cost of the treatment?

Let us unpack these one by one.

2.2.1 Likelihood of utilising non-CDL

Analysis of patient behaviour in the final quarter of 2022 indicates that utilisation of non-CDL treatments was significantly higher in private hospitals compared to public healthcare institutions.

By 2024, the Ministry of Health noted that over 90% of new cancer patients in Singapore were receiving treatments listed on the CDL, suggesting that clinical pathways were rapidly aligning with the positive list.

The underlying cause of the higher non-CDL utilization in private hospitals - roughly double that of the public sector - stems from a greater clinical preference for novel, late-stage, or off-label therapies that may not yet meet the cost-effectiveness thresholds required for the CDL.

2.2.2 Likely Duration Of Treatment & Estimated Cost

Should the use of non-CDL drugs be warranted, the next concern that we would have would be the estimated total cost of treatment.

(Disclaimer: I am not medically trained, and the information presented is the understanding from a layman’s secondary research.)

From what I’ve gathered, these are the non-CDL drugs that can and are prescribed to treat common cancers such as: Breast, Prostate, Colorectal, Lung, Lymphoma, Leukaemia, Liver and Bladder.

For treatment that runs continuously until progression, the question that we need to ask is “how long does it take for us to assess if any progression is made”? Based on my understanding, that would usually take around 8 to 13 months.

Personal Verdict: Based off this understanding, coupled with the estimated monthly/dosage cost of the various commonly prescribed non-CDL drugs, having a non-CDL coverage does seem to be an important consideration given the high financial burden associated with the treatment.

2.3 Verdict For The Use Case For Newer Riders

From our above two exercises, it is clear that the value of having an Integrated Shield Plan Rider now lies solely with the coverage of non-CDL treatments and not so much the provision of deductible (older rider) or co-insurance cap coverages.

Having this understanding is important as it dictates what the best action moving forward is when it comes to the provision of health care financing in Singapore.

This brings me to the last section.

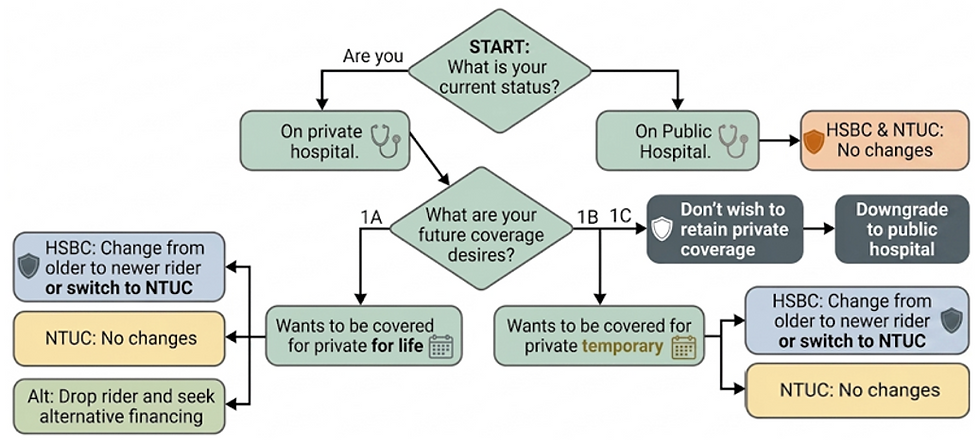

3. Actions You Can Consider

Now that we have a clear understanding of what’s changed, here are the corresponding actions that you can consider depending on your view and preferences towards the provision of your health care financing in Singapore.

Before we get into it, let me just indicate the lifetime cost of maintaining the ISP riders from 30 to 65/75/85 years old as these will heavily impact our decision-making process.

It is also important to highlight that for the areas of non-CDL, the benefits between HSBC Life and NTUC Income are quite different:

In a nutshell, depending on your status and preferences, these are the respective choices you can consider:

3.1 Covered for Public Hospital

I’d recommend that you retain the older rider as the benefits of having your deductibles covered and having a lower co-payment cap is worth paying for given the negligible difference in premiums between the current and older rider. (One episode will break even on the cost differential)

3.2 Covered for Private Hospital (HSBC Life)

If your current health and medical record is clean, I’d recommend that you consider that you either change to the current rider if you value a higher non-CDL coverage or switch to NTUC income for cost savings but be covered lesser for non-CDL.

If your have a pre-existing condition that is covered by HSBC Life, I’d recommend that you consider changing to the current rider for the cost savings as switching may not be an option to pursue unless you’re prepared for exclusion on your pre-existing condition that is currently covered under HSBC Life.

If your intention is to be covered for private temporary and eventually downgrade to Public A ward, I’d recommend that you stay on HSBC Life as the non-CDL coverage difference that they provide for A ward coverage is significantly higher than NTUC income and the cost differential is not unreasonable.

3.3 Covered for Private Hospital (NTUC Income)

As the cost leader of the industry, no action is recommended if you are on NTUC income.

3.4 Don’t Have a Strong Want for Private Coverage

If you’re on the fence between Private & A ward Hospitalization coverage, am covered for Private Hospitalization coverage but cannot tolerate the high and in the future higher premiums, I’d recommend that you consider downgrading to Public A ward hospital.

The reason is that if you’re feeling the emotional or financial pinch today, this feeling will only get worse in the future, and the likely outcome is that you’ll eventually downgrade when approaching your retirement age, as it is unlikely that you’ll make provisions for financing the private hospitalization cost during your retirement.

3.5 Want To Be Covered For Private But Don’t Want To Pay For Rider

If you wish to be covered for private hospitalization treatment but feel that the rider may not be worth paying for, there are two options available to you.

The most obvious one would be to terminate the rider but doing so would mean that the risk of financing for non-CDL treatment is going to be coming out 100% from your assets which also means that you need to make additional provisions for your retirement planning to provide for potential health care financing.

If you wish to make provisions for non-CDL items but do not wish to use the rider for it, the recommendation would be to utilise a life insurance with critical illness coverage that lasts minimally until the age of 85.

Doing so ensures that you’ll have the payout necessary to finance the non-CDL treatment while retaining the flexibility in the utilization of the coverage and enjoying a higher probability of claim as Critical Illness encompasses more than just Cancer as opposed to the non-CDL treatment coverage which is very niche and specific.

While the lifetime cost of using a whole-life insurance is similar if not lower than that of a hospitalization rider, financing your non-CDL coverage using a life insurance does carry some level of risk as well.

The biggest risk deals with the scenario where a long term non-CDL treatment is necessary as your life insurance payout will not be able to out last the sheer amount of cost that you’ll have to bear, leaving you with a potential gap in financing.

That said, from an expected return standpoint (Probability of claim * payout amount), I’d argue the expected return from utilising a life insurance is much higher than that of a shield plan rider largely due to the probability of claim.

Below is a breakdown of the consideration and comparison between both modes of financing.

PLEASE SEEK FINANCIAL ADVICE TAKING ANY ACTION. Whatever presented in this article is merely my opinion and is not financial advice.

4. Actions I'm Taking For Myself

As I’m currently on HSBC Life Private Hospitalization coverage and I want to be covered for Private Hospital treatment, here are the actions I’ll be taking.

Firstly, given that I already have an ongoing whole-life plan, the lower non-CDL coverage is something that isn’t much of an issue to me and I’ve decided to hop over to NTUC income for the purpose of cost savings.

Secondly, to hedge against any future hospitalization changes and nerfs, I’ll be buying another whole-life plan with a lifetime coverage of $400,000. Doing so ensure that minimally, I’ll be covered at $500,000 in life insurance for life while having a decent amount of hospitalization coverage.

Should the value hospital insurance riders continue to deteriorate in the future, I will be in a position that allows me to just drop the rider completely while having sufficient coverage from the life insurance to finance for any non-CDL treatment.

By switching to NTUC income and adding on another whole-life insurance, I’ve made sure that my ultimate downsides are fully hedged while maximising the expected returns (or payout) of my insurance portfolio.

In the worst possible scenario where I’ve dropped the shield plan rider and a non-CDL treatment must be administered, I’ll be pursuing the treatment within the government A ward hospital to keep the cost manageable and to stretch my payout.

Based on the research, the average duration of treatment would be around 24 to 48 months of which the assessment period of the effectiveness of treatment would span an average of around 8 to 13 months.

In other words, in the situation where a full effective treatment is warranted, the likely damage from non-CDL in Public A Ward hospital (assuming $15,000 per month) would be around $360,000 to $720,000. This is within my comfort zone based on my $500,000 to $600,000 life insurance payout then.

In the best-case scenario where nothing happens to me in my lifetime, the payout from my life insurance will be taken into consideration in my legacy planning for my children.

Daniel is a Licensed Independent Financial Consultant with MAS and a Certified Financial Planner (CFP®).

Connect with me on social media platforms to receive updates on future content! You can also slide into my DMs if you have any questions :)

Disclaimer:

This article is meant to be the opinion of the author

This article is for information purposes only

This article should not be seen as financial advice

This advertisement has not been reviewed by the Monetary Authority of Singapore

![Is Prime US REIT A Good Buy In 2026? [Fundamental Analysis]](https://static.wixstatic.com/media/5dc7f7_cb0744a6711b4e5a8d42195c36c70474~mv2.png/v1/fill/w_1277,h_720,fp_0.50_0.50,q_35,blur_30,enc_avif,quality_auto/5dc7f7_cb0744a6711b4e5a8d42195c36c70474~mv2.png)

![Is Prime US REIT A Good Buy In 2026? [Fundamental Analysis]](https://static.wixstatic.com/media/5dc7f7_cb0744a6711b4e5a8d42195c36c70474~mv2.png/v1/fill/w_972,h_548,fp_0.50_0.50,q_95,enc_avif,quality_auto/5dc7f7_cb0744a6711b4e5a8d42195c36c70474~mv2.png)

![Is Alpha Integrated REIT A Good Buy In 2026? [Fundamental Analysis]](https://static.wixstatic.com/media/5dc7f7_9e65dba84d3241c394c403cd426c71c3~mv2.png/v1/fill/w_1277,h_720,fp_0.50_0.50,q_35,blur_30,enc_avif,quality_auto/5dc7f7_9e65dba84d3241c394c403cd426c71c3~mv2.png)

![Is Alpha Integrated REIT A Good Buy In 2026? [Fundamental Analysis]](https://static.wixstatic.com/media/5dc7f7_9e65dba84d3241c394c403cd426c71c3~mv2.png/v1/fill/w_972,h_548,fp_0.50_0.50,q_95,enc_avif,quality_auto/5dc7f7_9e65dba84d3241c394c403cd426c71c3~mv2.png)

![Is Keppel DC REIT A Good Buy In 2026? [Fundamental Analysis]](https://static.wixstatic.com/media/5dc7f7_67bdd0860d0846c88414003d90cc03f1~mv2.png/v1/fill/w_1277,h_720,fp_0.50_0.50,q_35,blur_30,enc_avif,quality_auto/5dc7f7_67bdd0860d0846c88414003d90cc03f1~mv2.png)

![Is Keppel DC REIT A Good Buy In 2026? [Fundamental Analysis]](https://static.wixstatic.com/media/5dc7f7_67bdd0860d0846c88414003d90cc03f1~mv2.png/v1/fill/w_972,h_548,fp_0.50_0.50,q_95,enc_avif,quality_auto/5dc7f7_67bdd0860d0846c88414003d90cc03f1~mv2.png)

Comments