[Market Updates] 2026 Quarter 1

- Daniel Lee

- Mar 31

- 9 min read

Updated: Apr 2

In my 2026 Market Outlook – I’ve expanded on the possibility of a high risk and high reward environment for 2026 driven by an improving confidence and demand for diversification towards Asia that could be offset by major cracks in the AI space and western economy.

Certainly, the inclusion of the risk of an escalating war in the Middle East and its consequences to the global economy is one factor that I did not anticipate.

In the first quarterly market update, I’d like to focus solely on

This will be a long ass update, so buckle up fam.

1. Timeline & Implications

The conflict unfolded with extraordinary speed across a five-week window.

What began as the largest US military buildup in the Middle East since the 2003 invasion of Iraq escalated — with little warning & bullshit reasoning — into a full-scale air war targeting Iran's political leadership, nuclear infrastructure, and military capacity.

The following chronology presents the defining events in sequence, providing the factual foundation for the economic and geopolitical analysis that follows.

Politics aside, the key implication of the ongoing war lies mainly in the effective closure of the Strait of Hormuz, its impact on crude oil prices, and thus on the prices of their derivatives.

1.1 What Is the Strait of Hormuz — And Why Does It Matter?

The Strait of Hormuz is a narrow waterway, just 34 kilometres wide at its narrowest point, separating Iran to the north from Oman and the United Arab Emirates to the south. Its two unidirectional shipping lanes facilitate the daily transit of approximately 20 million barrels of oil — roughly 20% of all the oil traded globally by sea.

As a result, the closure of the strait has been described by the International Energy Agency as the 'greatest global energy security challenge in history' — surpassing even the 1973 Arab oil embargo in absolute barrels disrupted, with the current crisis stranding approximately 15.8 million barrels per day.

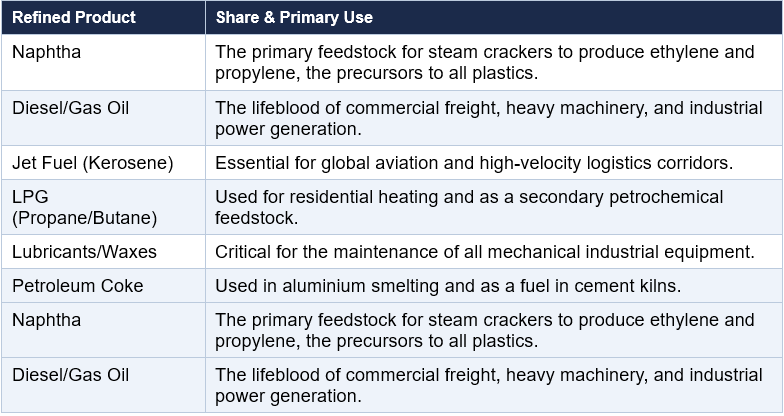

1.2 Crude Oil: The Lifeblood of the Modern Economy

To understand why a disruption in the Strait of Hormuz ripples so profoundly through global markets, one must first appreciate the foundational role crude oil plays in virtually every sector of the modern economy.

Crude oil is not merely fuel for cars and aeroplanes — it is also a part of the raw material from which thousands of downstream products are manufactured.

This means that a sharp and sustained increase in the price of crude oil does not stay confined to merely shipping & transport costs. It propagates through supply chains with a lag of weeks to months, raising the production cost of nearly every manufactured good.

The most significant of these are nitrogenous fertilisers and helium, both of which are deeply integrated into the natural gas and oil extraction processes of the Persian Gulf.

The Persian Gulf region serves as the primary valve for global agricultural stability, producing nearly half of the world's seaborne urea and 30% of its ammonia. The current blockade has already triggered a 50% surge in urea prices, a shock that is expected to drive global food inflation up by 3.1% as crop yields decreases.

Simultaneously, the forced shutdown of Qatari facilities has paralyzed 30% to 38% of the global helium supply. Because helium is irreplaceable in the cooling and lithography processes of semiconductor fabrication, this shortage directly threatens the production of High Bandwidth Memory (HBM) chips.

Given the global economy's burgeoning reliance on the AI industry, any sustained 'hiccup' in chip output could significantly cap the pace of global technological and economic growth through 2026 and 2027.

1.3 Implications

The ongoing conflict has fundamentally altered the global economic outlook, shifting the narrative from a path of stronger growth to one of systemic instability and stagflationary risk.

The following summary outlines the primary global implications:

Elevated Global Inflation: The surge in energy and commodity prices has forced a sharp upward revision of inflation forecasts. G20 inflation is now projected to be 1.2 percentage points higher than previously expected, reaching 4% for the full year 2026. In the United States, headline inflation is forecast to hit 4.2%, while global food prices are expected to rise by at least 3.1% due to the direct impact of fertiliser shortages on crop yields.

"Higher for Longer" Interest Rates: Central banks have been forced to pivot away from planned easing cycles to combat supply-driven inflation. The European Central Bank has already postponed its scheduled interest rate reductions, citing "profound uncertainty" regarding energy prices. Similarly, the U.S. Federal Reserve is expected to keep the Fed funds range steady at 3.5%–3.75% through at least 2026 to manage sticky inflation and build price pressures.

Deepening Regionalism and Supply Chain Diversification: The "Hormuz Blockade" has accelerated a structural shift away from globalised efficiency toward regional resilience.

North America: The United States and Canada are leveraging the 2026 USMCA review to deepen continental energy and technology integration, positioning the region as a "net-exporter fortress".

Asia: China and India are aggressively exploring alternative overland corridors and "friend-shoring" partnerships. This includes accelerating the "Power of Siberia 2" pipeline with Russia and expanding the use of the Northern Sea Route to bypass maritime chokepoints.

Industrial Re-alignment: Manufacturers are abandoning "just-in-time" inventory models in favour of strategic operational buffering and "friend-shored" sourcing for critical materials like resins and semiconductors to mitigate future blockade risks.

2. Different Scenarios Moving Forward

Unlike the trade war launched by Donald Trump last April, the current war in Iran isn’t something Trump can easily “chicken out” of, as the decision to “de-escalate” now lies with not just the aggressors but also the defenders (Iran) themselves.

Even if the aggressors decide to stop their aggression and initiate a self-proclaimed ceasefire, Iran can easily continue to bomb critical infrastructures in the Gulf and keep the Straits closed unless they are incentivised to do otherwise.

In my opinion, here are the 3 most likely scenarios that may materialize with regards to the ongoing conflict – looking at how things are transpiring, scenario 1 & 3 seems to be the most likely scenarios that may materialise.

Scenario 1: Boots On The Ground (Escalation)

In this scenario, the U.S. and Israel conclude that aerial dominance and "decapitation" strikes have failed to break Iran's chokehold on the Strait of Hormuz. Following the deployment of the 2,500-3,500 Marines specialised in amphibious landings, the coalition initiates "boots on the ground" operations to seize Kharg Island or establish beachheads along the Iranian coast.

The outcome: Iran follows through on its promise to "set American soldiers ablaze," transitioning the conflict into a war of attrition. Pro-Iranian militias in Iraq and the Houthis in Yemen expand their targeting to desalination plants and city centres across the GCC, turning the region into an unlivable "zone of departure" for the 90% expatriate workforce.

Scenario 2: “Guaranteed” Off-Ramp (3rd Party Mediation)

This scenario assumes a "mutually hurting stalemate" where the U.S. faces domestic political pressure from $5-per-gallon gasoline, and Iran's military capabilities are significantly degraded. Pakistan, leveraging its 900km border and ties to both sides, hosts a summit involving Egypt, Turkey, and Saudi Arabia to broker a ceasefire.

The outcome: Pakistan acts as the intermediary, but a “security guarantor" will be necessary. A deal is struck where Iran reopens the Strait in exchange for the removal of certain oil sanctions and "firm international guarantees" against future leadership assassinations. However, the issue with this scenario right now is that there doesn’t seem to be a country that can and is willing to step up and fulfil the role of a security guarantor in an increasingly volatile region.

Scenario 3: The New Abnormal (Persistent Blockade)

The conflict enters a state of "soft closure" where neither a full ground invasion nor a diplomatic breakthrough occurs. Iran maintains a selective blockade, allowing only "friendly" vessels (Chinese, Indian, or Pakistani flagged) to pass, while targeting Western-linked shipping with drone swarms and mining.

The outcome: The world effectively splits into two energy spheres. The "North American Fortress" becomes self-sufficient through deeper USMCA integration and Canadian oil sands output. Meanwhile, China and India are permanently pivoting toward overland Russian pipelines and the Northern Sea Route, accelerating the "Petroyuan" to bypass the U.S. dollar-dominated maritime insurance system.

3. Likely Impact of Scenarios 1 & 3

Given that scenario 1 & 3 have the highest probability of occurring, here are their impacts in General, North America & Europe and in Asia/Emerging markets.

Scenario 1: Boots On The Ground (Escalation)

General (Global)

Collapse of the GCC Model: The Gulf Cooperation Council (GCC) economic model, built on political stability and diversification, faces systemic collapse. Hostilities render major aviation hubs (Emirates, Qatar Airways) and logistics centers like Jebel Ali non-functional.

North America & Europe

United States Resilience and Cost: The U.S. economy is buffered by domestic production (13.6 mb/d), but faces a "stagflation-lite" outlook. Direct war costs exceeding $200 billion put extreme pressure on the national budget, potentially forcing the Federal Reserve to abandon planned interest rate cuts and even exploring rate hike if the employment market permits.

Europe's Existential Threat: Europe faces a severe energy-supply shock and industrial strain. The Eurozone economy is projected to contract in Q2 2026, with the European Central Bank (ECB) potentially raising interest rates to combat 0.5–1.0% additional inflation.

Asia & Emerging market

High-Tech Industrial Crisis: Japan and South Korea are the most vulnerable, sourcing 85–87% of their oil via the Strait. South Korea’s semiconductor sector faces a "double blow" from rising energy costs and the loss of Qatari helium essential for chip manufacturing.

Humanitarian Burden/Opportunity: The mass exodus of millions of workers from the Gulf creates a repatriation crisis. In the short term, this poses social and economic challenges as there is more demand for an already shrinking supply of resources caused by the crisis within the region. That said, if managed well, the flow of capital and human resources may present itself to be an opportunity for Asia & Emerging markets to capitalise on as they become factors of long-term growth.

Scenario 3: The New Abnormal (Persistent Blockade)

General (Global)

Financial and Insurance Rupture: Global P&I clubs have abrogated war-risk coverage for the Persian Gulf. This "actuarial warfare" makes maritime transit prohibitively expensive, with premiums rising to 5–10% of vessel value which will likely be transferred to consumers in the form of higher-end good prices.

Petroyuan Acceleration: Sanctions and blockades push global energy trade toward a "petroyuan-leaning nexus". Yuan transactions already account for 42% of Moscow’s currency trades, and the Shanghai INE is emerging as a primary hedging tool for Asian physical flows.

North America & Europe

The North American Fortress: Deepened USMCA integration focuses on a regional supply chain security mechanism to protect critical goods. The U.S. and its partners prioritise Western Hemisphere dominance over Eurasian stability, effectively creating an energy-independent "fortress".

Industrial Realignment: European and North American chemical producers are hastening a shift toward U.S.-sourced ethane and LPG to avoid Middle Eastern chokepoint risks.

Asia & Emerging market

The Asian Energy Pivot: China and India are permanently pivoting toward overland Russian pipelines and the Northern Sea Route (NSR). NSR transit shipping reached 3.2 million tons in 2025, dominated by oil flows between China and Russia.

Regional Fragmentation: While China leverages strategic reserves and alternative routes, more price-sensitive emerging markets (Pakistan, Bangladesh) face severe fuel shortages and localized economic crises. This presents an opportunity for regional powerhouse like China to step up and expand their regional influences via economic aid provided that they are able to manage their own domestic challenges.

Long Story Short

The 2026 Iran conflict marks the end of the globalised "Oil for Security" era.

Scenario 1 demonstrates that a full military escalation would devastate the GCC economic model and trigger acute stagflation in Europe and high-tech Asia.

Scenario 3 suggests that even without a total war, a persistent "soft blockade" will permanently bifurcate the global economy into a dollar-denominated Western fortress and a yuan-leaning Asian energy nexus.

Regardless of which scenario materialises, what is certain is that the future global market will likely prioritise geographic resilience and decentralised energy production over the cost-optimised efficiency of the previous decades.

From a probabilistic standpoint, as compared to the start of the year, the probability of a persisted correction is much higher than a V-shaped recovery in 2026. The question now is how bad the situation will be and when the economic impact will materialise in the data (usually around 3 to 6 months).

Careful observers will realise that while the short term developments may seem bleak, not all is lost in the long term as this event will once again strengthen the resolve and needs of Emerging and Asian countries to deepen trade relationships to enhance their economic resilience which is a factor of a sustained long-term growth.

As what the Western propaganda is preaching: Short-Term Pain For Long Term Gain.

Though in this case, this seems to be only true for most of the countries apart from the United States, which unleashed this chaos upon the world and will be experiencing an ex-US diversification trend by the rest of the world.

As usual, only time will tell.

If you have any questions, you can PM me anytime. If not, I’ll catch you on our annual review.

Daniel is a Licensed Financial Consultant with MAS and a Certified Financial Planner (CFP®).

Connect with me on social media platforms to receive updates on future content! You can also slide into my DMs if you have any questions :)

Disclaimer:

This article is meant to be the opinion of the author

This article is for information purposes only

This article should not be seen as financial advice

This advertisement has not been reviewed by the Monetary Authority of Singapore

![Is Alpha Integrated REIT A Good Buy In 2026? [Fundamental Analysis]](https://static.wixstatic.com/media/5dc7f7_9e65dba84d3241c394c403cd426c71c3~mv2.png/v1/fill/w_1277,h_720,fp_0.50_0.50,q_35,blur_30,enc_avif,quality_auto/5dc7f7_9e65dba84d3241c394c403cd426c71c3~mv2.png)

![Is Alpha Integrated REIT A Good Buy In 2026? [Fundamental Analysis]](https://static.wixstatic.com/media/5dc7f7_9e65dba84d3241c394c403cd426c71c3~mv2.png/v1/fill/w_972,h_548,fp_0.50_0.50,q_95,enc_avif,quality_auto/5dc7f7_9e65dba84d3241c394c403cd426c71c3~mv2.png)

![Is Keppel DC REIT A Good Buy In 2026? [Fundamental Analysis]](https://static.wixstatic.com/media/5dc7f7_67bdd0860d0846c88414003d90cc03f1~mv2.png/v1/fill/w_1277,h_720,fp_0.50_0.50,q_35,blur_30,enc_avif,quality_auto/5dc7f7_67bdd0860d0846c88414003d90cc03f1~mv2.png)

![Is Keppel DC REIT A Good Buy In 2026? [Fundamental Analysis]](https://static.wixstatic.com/media/5dc7f7_67bdd0860d0846c88414003d90cc03f1~mv2.png/v1/fill/w_972,h_548,fp_0.50_0.50,q_95,enc_avif,quality_auto/5dc7f7_67bdd0860d0846c88414003d90cc03f1~mv2.png)

![Is Elite UK REIT A Good Buy In 2026? [Fundamental Analysis]](https://static.wixstatic.com/media/5dc7f7_9c26044789c94d87bee2977f637553a9~mv2.png/v1/fill/w_1277,h_720,fp_0.50_0.50,q_35,blur_30,enc_avif,quality_auto/5dc7f7_9c26044789c94d87bee2977f637553a9~mv2.png)

![Is Elite UK REIT A Good Buy In 2026? [Fundamental Analysis]](https://static.wixstatic.com/media/5dc7f7_9c26044789c94d87bee2977f637553a9~mv2.png/v1/fill/w_972,h_548,fp_0.50_0.50,q_95,enc_avif,quality_auto/5dc7f7_9c26044789c94d87bee2977f637553a9~mv2.png)

Comments